Many eyes are on Texas this summer. Some are watching the Houston Astros to see if a repeat of the 2017 season is possible; currently they are leading the American League West by 6 games and occupy the number 2 spot in USA Today’s Power Rankings. I cannot report similar good news for the Atlanta Braves, although hope springs eternal.

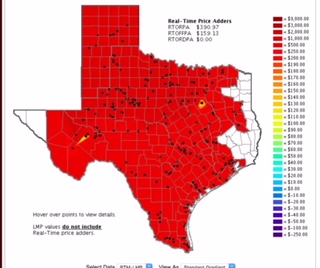

However, those lucky enough to have a professional or avocational (yes, that is a word) connection to the energy industry are collecting a different set of stats by following the state’s roller coaster of summer peak temperatures and power prices. Some notable records have been set. For example, last week in Dallas, day-ahead spot prices for electricity hit $841/MWh. Normally, wholesale prices across the state range from $10 to $50/MWh.

Even last year, experts at ERCOT and across the state flagged some concerns about reserve margins. As the Houston Chronicle reported, “ERCOT in 2010 adopted guidelines calling for the grid’s generating capacity to exceed demand by at least 13.75 percent.” ERCOT’s December 2017 forecast estimated 2018 summer reserve margins of less than ten percent. A key reason was the pending retirement of three coal plants and one natural gas plant that formerly supplied 4,300 megawatts.

On Monday, peak demand topped out at 71,444 MW between 5 and 6 pm. Luckily, no brownouts have occurred, but at times in this long, hot month, the actual reserves have fallen to 2,000 MW. That’s one or two power plants away from trouble. You can follow ERCOT on Twitter (I’m guessing their tweet stream has set a summer volume record) or, if you are wondering if there will be enough power to watch major league baseball on TV, check their daily reserve margin report.

How can this be? After all, Texas is the Saudi Arabia of wind! It has an enviable and ample transmission system. But, supply and demand still matter, and so does the dispatchability (if it’s not a word, it should be) of resources.

During some of the hottest hours and at times of peak demand, the Texas wind became a slow, fickle breeze, often contributing less than ten percent to the power flow. That means the state’s coal, nuclear and natural gas units have once again carried Texans through a precarious period. And while this summer has been notable, it really is just continuing a long-standing trend. Non-wind generation provides most of the power Texans need on summer and winter peak days.

What do high spot prices, low reserve margins and marketplace drama mean for consumers? Low-cost deals, often touted as the driver for retail deregulation, are disappearing like the wind. In June, the Houston Chronicle reported that “[c]onsumers hoping to find better deals when their electricity contracts expire are in for a shock as retail prices have soared in anticipation of hot weather, potential power shortages and spikes in wholesale electricity prices. The low teaser rates for consumers available just a month ago have disappeared.”

Why are traditional baseload plants disappearing - and being replaced by wind - when there is clearly a need to keep them? The answer is longer than a major league double-header and more complicated than one PACE blog can accommodate. Look for more baseball tie-ins and answers to these questions next week and in several presentations we’re making across the country this summer.

{kind=link}